Simplifying my portfolio (pt 1): questioning the small cap fund

· 1066 words · 6 minutes read

Simplifying my portfolio

Of all the decisions that I made since I started investing, the one that I regret the most concerns the complexity of my portfolio. It consists of 5 different funds, meaning the broker fees that I pay for each investment round are high.

In this series of articles I intend to investigate simplifying my portfolio. I will assess the role of each of its equity funds to determine whether or not I can remove the fund without affecting exposure or performance. If not, could I merge it with another fund?

The rule of thumb says that you shouldn’t spend more than 0.5% of your annual investments on transaction fees. I contribute €200 per month to my investments, meaning I shouldn’t spend more than €12 per year on broker fees.

My broker, Lynx, charges a minimum of €6.00 per transaction. Because my portfolio has 5 funds, I spend €30 each investment round on broker fees alone. Even if I invest only once per year, this is more than I should spend. The fees are too high compared to my contributions and this will reduce the performance of the portfolio in the long term.

The role of the small cap fund

In this first article, we are going to scrutinize the role of the small cap fund in my portfolio.

| ETF | Type | Allocation |

|---|---|---|

| Xtrackers Global Government Bond EUR Hedged | Bonds | 18% |

| iShares Core MSCI World | Stocks | 49% |

| ➡️ iShares MSCI World Small Cap | Stocks | 14% |

| Xtrackers MSCI Emerging Markets | Stocks | 10% |

| Amundi ETF FTSE EPRA NAREIT Global | Real-estate | 9% |

The problem with small cap stocks

In 1981, Banz published a paper1 where he found evidence of a “size effect”. By analyzing the US stock market between 1936 and 1975, he found that smaller firms on average had higher risk adjusted returns than larger firms. Since then, small cap stocks have been regarded as deserving of their own allocation in a diversified portfolio, next to other types of equities such as large cap stocks. This was the basis for the presence of the small cap fund in my portfolio.

But recently his findings got debunked. Researchers recreated the study in 20182 using today’s data and found:

- The size effect that Banz discovered was statistically weak. His research barely meets the 10% significance threshold and does not meet the more commonly used threshold of 5%.

- They could not replicate the size effect across different time periods and geographies.

The size effect does not really exist, so does this mean that we should get rid of small cap stocks from our portfolio?

Value stocks at the rescue

A different pattern emerges when we make a distinction between value and growth stocks. It turns out that growth small cap stocks are responsible for the underperformance and statistical unreliability of the asset class as a whole3. In other words, if we remove growth small cap stocks, the size effect comes back to life. It becomes consistent over time and across geographies, delivers a larger premium and it becomes statistically significant.

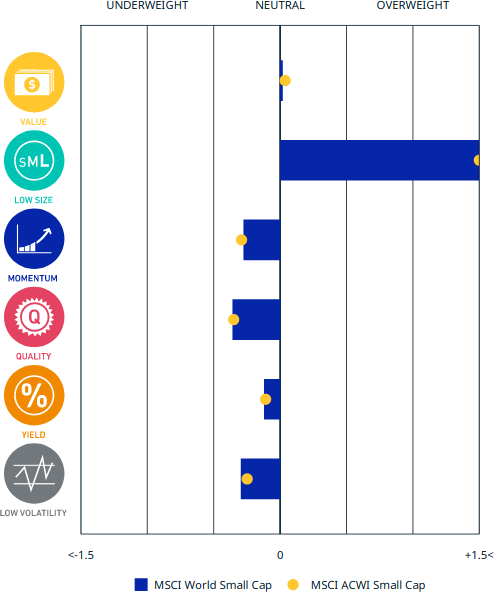

Composition of MSCI World Small Cap

The small cap fund in my portfolio, iShares MSCI World Small Cap, tracks the MSCI World Small Cap index. We expect the index to hold both value and growth stocks. Indeed, the image below shows that it holds about an equal amount of value and growth stocks, with only a negligible tilt towards value stocks.

Factors of the MSCI World Small Cap index (source: factsheet)

Performance of MSCI World Small Cap Value

The research tells us that we’re better off getting rid of the small cap fund unless we find a way to remove growth stocks from the small cap index and keep only value stocks. MSCI has an index that does that: the MSCI World Small Cap Value index.

Let’s find out how the MSCI World Small Cap variants have compared to each other in the past:

Evolution of the MSCI World Small Cap variants (source: Backtest)

A backtesting period of 20 years is statistically insignificant. But it’s encouraging because it confirms the research: the premium as a result of the size effect is larger for value small cap stocks than for growth small cap stocks.

Finding a global value small cap index

Great! So all we have to do is replace our small cap fund with a fund that tracks a global small cap value index. Unfortunately, this is where the good news ends.

A search on justETF for all small cap equity funds yields the following indexes:

- EURO STOXX Small

- MSCI AC Far East ex Japan Small Cap

- MSCI EMU Small Cap

- MSCI Emerging Markets Small Cap

- MSCI Europe Small Cap

- MSCI Europe Small Cap Value Weighted

- MSCI Japan Small Cap

- MSCI UK Small Cap

- MSCI USA Small Cap

- MSCI USA Small Cap Value Weighted

- MSCI World Small Cap

- Russell 2000

- S&P SmallCap 600

- SDAX

- STOXX Europe Small 200

We are looking for an index that is global and contains only value stocks. None of these indexes match these criteria.

Verdict: drop the small cap fund

We face a situation where the ideal solution, a fund tracking the MSCI World Small Cap Value index, does not exist in practice. The research shows that the size premium does not exist when including growth small cap stocks, which is the case for the MSCI World Small Cap index. So until a small cap value fund becomes available, we’re better off dropping the small cap fund from our portfolio altogether.

Updated portfolio

This decision liberates 14% of my portfolio. I don’t want to change the bond/equity ratio so I’m not going to allocate a higher percentage to the bond fund. Also, I’m reticent on giving more exposure to real estate or emerging markets. That’s why I’m going to allocate more to the MSCI World fund, its large cap counterpart.

Now, we’ve obtained a simpler portfolio:

| ETF | Type | Allocation |

|---|---|---|

| Xtrackers Global Government Bond EUR Hedged | Bonds | 18% |

| iShares Core MSCI World | Stocks | 63% |

| Xtrackers MSCI Emerging Markets | Stocks | 10% |

| Amundi ETF FTSE EPRA NAREIT Global | Real-estate | 9% |

Acknowledgments

I would like to thank Ben Felix. His excellent video The Problem With Small Cap Stocks presented the research that provided the basis for my conclusions. Furthermore, I highly recommend his entire YouTube channel!